Wednesday, September 19, 2007

Thursday, August 30, 2007

Are those new or old waves?

On September 6th, the United States Department of Justice (DJ) submitted an ex parte filing regarding the regulation of the traffic over the Internet, in the context of what have been the so called "net neutrality" rules.

On September 6th, the United States Department of Justice (DJ) submitted an ex parte filing regarding the regulation of the traffic over the Internet, in the context of what have been the so called "net neutrality" rules. In the document, the DJ advices that the Federal Communications Commission (FCC) "should be highly skeptical of calls to substitute special economic regulation of the Internet for free and open competition enforced by antitrust laws", arguing that the proponents of neutrality propose marketplace restrictions could prevent, rather than promote, optimal investment and innovation in the Internet, having thus negative effects for the economy and consumers.

The Act of 1996, passed by the American Congress to "promote competition and reduce regulation (...) encourage the rapid development of new telecommunications technologies" is also mentioned as argument "against" neutrality.

The report refers to proponents of "net neutrality" regulation as failing to "show that a sufficient case exists for imposing the sorts of broad marketplace restrictions that have been proposed", and points three examples why neutrality has the potential to harm consumers: 1- By precluding broadband providers from charging fees for priority service could drift the entire burden of implementing costly network expansions and improvements onto consumers. 2- Mandating a single, uniform level of device for all content could limit the quality and variety of services that are available to consumers and discourage investment in facilities. 3- Proposed regulations could unreasonably limit the ability of broadband providers to manage their networks efficiently.

The ex parte calls the attention to "the increased usage and popularity of new services that are sensitive to delays in delivery (...) has increased demand for bandwidth. In response, broadband providers have made, and continue to make, significant investments in Internet infrastructure to meet rising demand and reduce Internet congestion". If we pick the analysis of the first post of The Telecoms, DJ is kind of aligned with the projection made in the Evernet scenario projected for Europe.

As a conclusion, DJ urges the FCC to exercise an adoption of rules that regulate the Telecoms sector.

As we know, one of the "fierce" proponents of "net neutrality" is the giant Google which does not own a physical infrastructure to carry its contents and services, and thus has to fight in the arena where Telecoms, IT, TV Broadcasters want to enter the business of each others. Google and other Internet companies have been accused, especially by AT&T and Verizon, of using their networks for free without any returns for them - which could configure a scenario where the infrastructure owners don't see any advantage on investing on new assets. On this subject, the DJ implicitly points that if neutrality was to happen, "that could force consumers (....) to bear the costs of maintaining and upgrading broadband providers' networks".

Google has been quite successful in creating (and in other cases by acquiring companies) products which are gaining momentum, such as GMail, Youtube, Google Maps, etc. All these products and services are using the Internet and MNOs networks to be carried.

During the last months, rumors of a Goggle Phone were spread in the news. Google is also in a race for spectrum which is to be free by 2009 because of DTT deployment. This can mean Google wants to provide their service using their own wireless assets.

Regarding the Google Handset, speculation points that GOOG wants to sell the cell phone and its own service plan - others talk about Google making a phone that transmits calls over the Internet rather than over cellular networks. However, these are just "Chinese whispers", but Google could for example buy air time in bulk from a carrier.

In what concerns the White space Google and others are fighting for, it has been a hot discussion. Google presents itself as a bidder in an upcoming auction of wireless spectrum and steer the creation of a new wireless broadband network. However, there's a condition, Google says it will participate if FCC would embrace its view on "net neutrality" - GOOG wants regulators to stipulate that the winner of the new spectrum gives consumers the freedom to use whatever mobile applications they desire on any handset they want; it also wants the winner to sell wireless services to resellers on a wholesale basis and let Internet-service providers interconnect with the network. Google had also made some trials/tests in the context of the White Spaces Coalition. This coalition consists of Microsoft, Google, Dell, HP, Intel, Philips, Earthlink and Samsung - it plans to deliver broadband access to consumers via existing "white spaces" in unused analog television frequencies. This is not good for TV Broadcasting industry which already launched an advertising campaign to fight against the white space use by claiming the devices to be used interfere with TV adjacent channels.

On the other front AT&T and Verizon, the bigger incumbents in USA, as expected are against Google (and there are rumors that Apple joined the race), on the grounds that the conditions are unfair to traditional wireless companies and would devalue the spectrum, depriving the government of billions of potential revenue.

Whatever the decision will be, there are some true facts - MNOs behave today in a quasi-monopoly market and disruption of wireless would be welcome for the final user and even for device manufacturers which in some cases need to make exclusive deals with MNOs. On the other end, Google is becoming the big storage of humans' records, rising thus concerns of privacy.

But one thing is for sure, from times to times the better is to shake the waves, shall they be new or old...

Sources: Cellular News, The Economist, Unites States Department of Justice, Wikipedia

Wednesday, July 18, 2007

Would you risk all your money in just one security?

Let's say you have a lot of money to invest. Would you risk all your money in just one security? If you would, if that security has some high level of risk, either you really know what you're doing (and then you are lucky) or there's a great probability to lose money. The same can be applied, in some extent, to the product/service portfolio of your company - that is known. Classical examples are that for example Motorola didn't choose a single operating system for their phones - it was one of the first to join the Symbian with Nokia and Ericsson. However, as we know, Motorola also launched Linux and Windows Mobile handsets. So the question is, is Motorola lost and doesn't know what it's really good? The answer is: right the opposite! As in financial portfolios, diversification can be beneficial. Of course there might be exceptions (e.g., you are a very specialized company and that is your strongest asset).

Let's say you have a lot of money to invest. Would you risk all your money in just one security? If you would, if that security has some high level of risk, either you really know what you're doing (and then you are lucky) or there's a great probability to lose money. The same can be applied, in some extent, to the product/service portfolio of your company - that is known. Classical examples are that for example Motorola didn't choose a single operating system for their phones - it was one of the first to join the Symbian with Nokia and Ericsson. However, as we know, Motorola also launched Linux and Windows Mobile handsets. So the question is, is Motorola lost and doesn't know what it's really good? The answer is: right the opposite! As in financial portfolios, diversification can be beneficial. Of course there might be exceptions (e.g., you are a very specialized company and that is your strongest asset). So, why is it important to diversify? First if one of you product fails, you have a chance with the other; then you develop expertise in more than one technology.

Given this, a management of this is strategically needed. That is especially true in what concerns innovation. It's also known that a very small amount of innovation experiences becomes a successful product/service. The questions here are "when shall you get out of some innovation", "what partnerships shall you take part in", "how many new projects shall you support"? These are questions without a straightforward answer, but looking to some successful companies, many practices show us that companies follow more than one standard (e.g. Orange provides OMA IMPS messaging service alongside with Microsoft Messenger in their handsets), some companies create partnerships which will drop latter (e.g., Motorola founded Symbian and is no longer one of the shareholders), and others promote creativity (HP gave one day time to employees for their own projects).

Even if we look the way R&D is done today, you'll see that companies no longer sit their researchers alone in a lab - they create several webs where clients and providers give inputs on their requirements so that research is also a collaborative work. This is good, because sometimes researchers like to work too long and own their innovations, leading sometimes to overlook and spend too much time to unsuccessful projects.

These paradigms need to be understood for R&D and innovation to be handled in a modern and efficient way. As someone one day told "marketing is too important to be in the hands of marketeers", maybe we can say "innovation is too important to be in the hands of innovators".

Thursday, April 26, 2007

Sexy telecoms

What are the features you find more important to choose a handset? Shall it look nice and sexy, shall it have the cutting-edge technologies, or is it simply because it has a nice price? Most probably the answer will depend on who you are, but one thing is for sure, 70%-80% of the non-voice revenues in 2006 came from SMS service. This means beyond doing voice calls, most of the people use handsets to send SMS, and thus, sophisticated services such as TV broadcast and location services (just to mention a few) are not really being used by people. Given that voice and SMS are the appliances that people really use, why is the telecom industry still looking for a "killer application"? A straightforward and consensual answer is that voice revenue margins are continuously eroding and fresh ideas that keep costumers connected are needed.

What are the features you find more important to choose a handset? Shall it look nice and sexy, shall it have the cutting-edge technologies, or is it simply because it has a nice price? Most probably the answer will depend on who you are, but one thing is for sure, 70%-80% of the non-voice revenues in 2006 came from SMS service. This means beyond doing voice calls, most of the people use handsets to send SMS, and thus, sophisticated services such as TV broadcast and location services (just to mention a few) are not really being used by people. Given that voice and SMS are the appliances that people really use, why is the telecom industry still looking for a "killer application"? A straightforward and consensual answer is that voice revenue margins are continuously eroding and fresh ideas that keep costumers connected are needed.As the mobile value chain is very fragmented, the industry founded some years ago OMA (Open Mobile Alliance) with the intent of creating interoperable applications. The number of applications standardized by this organization body is huge and it involves the latest advanced technologies. However, it seems adoption of these technologies is slow and revenues mobile operators get from them accounts for a very small part of the pie.

So what's the main "problem" with that? Are these applications expensive to develop or are network operators charging too much for the services they provide? Maybe the answer is both! Some researchers point that mobile phone industry is becoming very similar to the PC industry. As we know, (and as in PC), companies are evolving from vertically integrated to integrators of parts (which are made from other more efficient companies). This is true in most technologies when interfaces between parts of a system become standardized and a single company is able to take advantage of economies of scale and expertise by doing just one part of the system. These kinds of companies are already part of the mobile value chain and some of them perform very well. Regarding the rates applied by MNOs, these new services are not deployed at a low cost, as companies cannot jeopardize themselves. However, it's becoming clear that network operators own an infrastructure that can carry all these applications' bytes. Some experiences are being held - for example, this month in Frankfurt you could subscribe a T-Mobile service that enables sending an MMS to e-mail addresses by a flat rate of €10. Thus, new price structures and utilization patterns will drive the adoption of mobile services.

However, what are the main forces that make people choose their mobile phone? In the developed countries, where purchasing power is higher, people tend to buy handsets for what they look like and not for the features or "complicated" applications they run. The top example is the Motorola RAZR which is a slim phone with an emphasis on design. Another example of this is the partnership between some mobile manufacturers and style brands - for example Motorola teamed with Dolce & Gabbana, and Vodafone with Ferrari. Another example could be Vertu (manufacturer of luxury handsets fully owned by Nokia) that are hand-crafted and where design and luxury are the differentiation factors.

So, maybe there is not a perfect approach but several approaches and the winner, as ever, is the one which delivers what the customer wants, because that... is sexy!

Wednesday, April 11, 2007

Network neutrality

Most of us have already heard about Network neutrality; there are several definitions for it, but the basic principles are: networks that don't favour some destinations over others, or classes of application (eg WWW) over others (eg online gaming or VoIP).

(...)

After making huge investments on building FTTx new networks across the US, companies such as AT&T and Verizon point their fingers to big internet companies by saying they are using their networks for free without any return for those carriers:

(...)

After making huge investments on building FTTx new networks across the US, companies such as AT&T and Verizon point their fingers to big internet companies by saying they are using their networks for free without any return for those carriers:

•AT&T CEO: “Google, Yahoo! are getting a free ride on AT&T expensive new network – we have spent a lot of capital and we have to have a return on it!”

•Verizon CEO: “Google, Microsoft and other providers ought to share the cost!”

(...)

On this discussion there are different positions to be taken - some argue networks shall be neutral and others don't. Arguments on the net neutrality side are accusing AT&T and Verizon for blocking innovation for start-ups and small companies.

(...)

Some opponents to net neutrality, put the question on a different angle; Odlyzko, University of Minnesota: “What makes them think that they are going to charge Google, as opposed to Google charging them?”

(...)

However, this discussion might not be new, fast broadband connections already cost more than slower, both for consumers and business. Given that carriers had put big money on new fast networks, on thing is for sure, or telecoms charge subscribers more or they pursue new business models where big internet companies and content providers pay part of the bill.

On this discussion there are different positions to be taken - some argue networks shall be neutral and others don't. Arguments on the net neutrality side are accusing AT&T and Verizon for blocking innovation for start-ups and small companies.

(...)

Some opponents to net neutrality, put the question on a different angle; Odlyzko, University of Minnesota: “What makes them think that they are going to charge Google, as opposed to Google charging them?”

(...)

However, this discussion might not be new, fast broadband connections already cost more than slower, both for consumers and business. Given that carriers had put big money on new fast networks, on thing is for sure, or telecoms charge subscribers more or they pursue new business models where big internet companies and content providers pay part of the bill.

Sunday, April 1, 2007

The Telecoms

IDATE and LECG (two consulting and research firms) had made public a study on Telecoms in Europe last January. The report was prepared for the Brussels Round table, a forum of leading EU telecommunications operators and equipment manufacturers that include Alcatel-Lucent, BT, Deutsche Telekom, Ericsson, France Telecom, Philips, Siemens, Telefonica and Telecom Italia.

This work analyses the current situation of the telecom industry along all its value chain as the sector contribution for the European economy.

Based on surveys made next to this industry’s key players, the main medium and long term driving forces that impact the industry are identified.

These main forces are:

- Changing end-user expectations, behaviours and usage patterns,

- Technology forces (telecoms, media and other tech fields),

- Globalization transitions,

- Regulation and public policy.

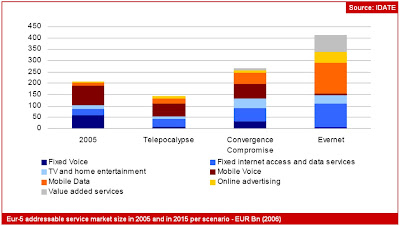

Given this environmental analysis, and based on the trends of the above mentioned forces, three possible scenarios for the 2015 European Telecom scene were built. As depicted in the figure below, telecoms can go as a trap (Telecopalypse), intermediate (Convergence Compromise) or favourable (Evernet). Each of this is characterized as follows:

This work analyses the current situation of the telecom industry along all its value chain as the sector contribution for the European economy.

Based on surveys made next to this industry’s key players, the main medium and long term driving forces that impact the industry are identified.

These main forces are:

- Changing end-user expectations, behaviours and usage patterns,

- Technology forces (telecoms, media and other tech fields),

- Globalization transitions,

- Regulation and public policy.

Given this environmental analysis, and based on the trends of the above mentioned forces, three possible scenarios for the 2015 European Telecom scene were built. As depicted in the figure below, telecoms can go as a trap (Telecopalypse), intermediate (Convergence Compromise) or favourable (Evernet). Each of this is characterized as follows:

Telecopalypse – For this scenario, there is a stagnation of the sector. It presents a situation were carriers might delay or cancel new network investments in face of policy regulations that favor network neutrality in opposition of application-based competition. The broadband availability is seen as modestly improved with low fiber and HDxPA deployed mainly in urban areas. The result is the telecoms transformed in a utility-like industry given the contracting industry-wide revenues.

Convergence Compromise - In this scenario high-speed fiber and mobile broadband is fuelled by infrastructure competition in dense urban areas in opposition to DSL coverage in less populated areas. Diffuse strategic choices are followed by operators, some focusing on Pan-European consolidation and fixed-mobile integration and others targeting the dedicated infrastructure provision. In this context, regulation is focused in ensuring retail-based competition through unbundling, facilities-based competition in dense urban areas, traffic prioritization and commercial freedom for converged services.

Evernet – The Evernet scenario introduces new services in the business-to-business and public administration domains (e-gov, e-health, machine-to-machine) generating cross sector productivity gains for the Euro economy. Broadband becomes a very important component for Europe, thanks to strong infrastructure competition resulting in the proliferation of multiple fiber and high broadband wireless access networks. Given this, the sector creates ample growth opportunities for both infrastructure and application providers. This scenario is possible in a context where a European public policy encourages cross-industry collaboration and a regulatory framework which stimulates fixed and mobile broadband facilities-based competition.

This report is issued in a time where the European telecom sector faces many challenges, such as market saturation (and maturation), deflation, regulation and competitive risk. It does not point any special direction and is not biased on a specific scenario. Although many of the variables studied can change in pace and direction, it gives a good outlook on the sector and important trends to look at.

The report can be downloaded here.

Subscribe to:

Comments (Atom)