This work analyses the current situation of the telecom industry along all its value chain as the sector contribution for the European economy.

Based on surveys made next to this industry’s key players, the main medium and long term driving forces that impact the industry are identified.

These main forces are:

- Changing end-user expectations, behaviours and usage patterns,

- Technology forces (telecoms, media and other tech fields),

- Globalization transitions,

- Regulation and public policy.

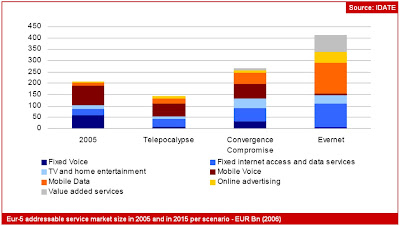

Given this environmental analysis, and based on the trends of the above mentioned forces, three possible scenarios for the 2015 European Telecom scene were built. As depicted in the figure below, telecoms can go as a trap (Telecopalypse), intermediate (Convergence Compromise) or favourable (Evernet). Each of this is characterized as follows:

Telecopalypse – For this scenario, there is a stagnation of the sector. It presents a situation were carriers might delay or cancel new network investments in face of policy regulations that favor network neutrality in opposition of application-based competition. The broadband availability is seen as modestly improved with low fiber and HDxPA deployed mainly in urban areas. The result is the telecoms transformed in a utility-like industry given the contracting industry-wide revenues.

Convergence Compromise - In this scenario high-speed fiber and mobile broadband is fuelled by infrastructure competition in dense urban areas in opposition to DSL coverage in less populated areas. Diffuse strategic choices are followed by operators, some focusing on Pan-European consolidation and fixed-mobile integration and others targeting the dedicated infrastructure provision. In this context, regulation is focused in ensuring retail-based competition through unbundling, facilities-based competition in dense urban areas, traffic prioritization and commercial freedom for converged services.

Evernet – The Evernet scenario introduces new services in the business-to-business and public administration domains (e-gov, e-health, machine-to-machine) generating cross sector productivity gains for the Euro economy. Broadband becomes a very important component for Europe, thanks to strong infrastructure competition resulting in the proliferation of multiple fiber and high broadband wireless access networks. Given this, the sector creates ample growth opportunities for both infrastructure and application providers. This scenario is possible in a context where a European public policy encourages cross-industry collaboration and a regulatory framework which stimulates fixed and mobile broadband facilities-based competition.

This report is issued in a time where the European telecom sector faces many challenges, such as market saturation (and maturation), deflation, regulation and competitive risk. It does not point any special direction and is not biased on a specific scenario. Although many of the variables studied can change in pace and direction, it gives a good outlook on the sector and important trends to look at.

The report can be downloaded here.

No comments:

Post a Comment